Despite offset accounts being around for years, there’s still many home owners who:

Despite offset accounts being around for years, there’s still many home owners who:

a) don’t know about them; or

b) have an offset attached to their home loan but aren’t using it properly.

We want to change that!

Below we explain what an offset account is and how if differs from a basic home loan. We also explain how to determine whether an offset account loan is something you could benefit from.

Basic loan vs loan with offset

A basic loan is exactly that – basic. It can either be a Variable Rate Loan or a Fixed Rate Loan, but it doesn’t have fancy features or rate discounts (because the rate is supposed to be already relatively low). Sometimes there’s a monthly account keeping fee payable.

Basic loans can be a good option if you have a relatively small loan and you want to keep things simple. For example, you’re keen on maintaining your everyday banking and savings accounts the way they are now (with the exception of making a monthly repayment to your new home loan).

Basic loans can work out to be financially advantageous if you don’t expect to build up surplus cash in an offset account and you just want to pay as much as you can directly into the loan itself. But it really depends on the rates that lenders are currently offering.

Variable Rate Loan with offset account option – “Professional Package”

A loan with the ability to link an offset account typically comes under a professional package.

A professional package is one that can:

- involve multiple loans (you might want to split your total borrowing into a fixed rate and variable rate loan for example)

- allow you to link one (or even multiple) 100% offset accounts to your variable rate loan

- incorporate other lender products – like a credit card, discounts off insurance etc

A yearly professional package fee replaces any monthly account keeping fees that can be charged on individual loans/offset accounts and credit cards. An annual package fee varies between lenders, but is generally in the vicinity of a few hundred dollars.

Whether you go for a basic loan or a professional loan package depends on two main things.

1. The rates available on either option

2. How much you intend to build up in your offset account (i.e. you want to anticipate enough interest savings from the offset account to warrant paying the annual package fee).

3. Consideration of your long term plans for the property. We won’t go into lots of detail here, but if you intend on moving out of your property at some point and renting it out, there’s a strong argument to use an offset account to preserve the future deductibility of debt, whilst still saving on interest costs whilst you’re living in the property. You may want to talk to your accountant about this one.

How does an offset account work?

Depending on your lender, an offset account typically works like a normal transaction account. You can deposit and withdraw funds whenever you like via EFTPOS, ATM, internet banking etc but because the offset account is linked to your loan, the balance of your offset account helps to reduce the interest you incur on your home loan.

Instead of earning interest on cash you have in a transaction account, you save interest at the rate you’re paying on your home loan.

The reason this works to your advantage is because the interest rate we pay on our home loans is generally higher than the rate we would earn on a savings account. This means that for no additional risk – and you have complete access to your funds at all times – your money is working harder for you.

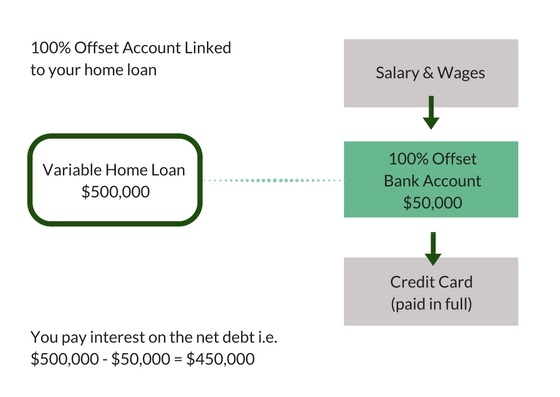

Here’s an example to explain.

If your $500,000 home loan was linked to a 100% offset account containing $50,000 cash, the lender charges interest on the net debt you owe (i.e. loan amount – balance of offset account = $450,000)

Let’s say your home loan has an interest rate of 6%p.a, with the rate on a normal savings account being 4%p.a. (Please note these are just examples and do not necessarily reflect current rates.)

On basic terms (not taking into compounding effects), this $50,000 could earn you $2,000 interest, if it stayed in a savings account for the whole year at a rate of 4%p.a.

Alternatively, if this $50,000 sat in an 100% offset account linked to your $500,000 home loan instead, you reduce your interest costs by $3,000 over the year.

If we compare the above options, you have saved $1,000 using an offset account instead of keeping your funds in a separate account. Furthermore, given you haven’t ‘earned’ any interest, there’s no interest income to report when you finalise your tax return for the year.

It’s important to note you don’t need to keep money ‘parked’ in an offset account to save interest. Most clients use their offset as an everyday banking account, but whilst funds sit there, they’re helping to reduce the home loan interest incurred.

*Please note this general information is provided as a guide only. You would need to refer to the PDS provided by your lender to ascertain specific information about any products offered by lenders.

- The Adviser Magazine · Young Broker of the Year (2016) - The Adviser Magazine · Mortgage Provider of the Year (2016, 2015) - REIACT · Finalist for Best Customer Service (2016) - MFAA · Young Broker of the Year (2015) - The Adviser Magazine · ACT/ NSW Business of the Year 6-10 loan writers (2015/2016)")